Running an indie bookstore means juggling thousands of SKUs, but rare books create their own operational nightmare. You've got a signed Kerouac sitting next to a mass-market paperback, both showing as "fiction" in your POS. Your part-timer just shipped that $850 illustrated Audubon in a bubble mailer because nobody flagged it as fragile. And when damage happens? You're scrambling through email threads trying to remember if you insured it, photographed it, or even logged its condition properly.

Most bookstores handle rare books like they handle everything else — until something expensive breaks. Then suddenly everyone's asking why there wasn't a proper rare book insurance SOP bookstore protocol in place. The real problem isn't that rare books need special handling. It's that without clear thresholds and workflows, every decision becomes a judgment call. Your team doesn't know what counts as "rare," your insurance coverage has gaps you haven't discovered yet, and when claims happen, you're reconstructing documentation that should've existed from day one.

Defining your rare threshold: price points that trigger different handling

The hardest operational decision around rare books is drawing the line. Where exactly does a book stop being regular inventory and start needing special protocols? Most stores never define this clearly, which means expensive books get missed or cheap books get over-handled.

Start with three tiers based on replacement cost, not retail price. Tier 1 covers books worth $150–500 — these need basic documentation but standard handling works fine. Tier 2 hits $500–2,000, where you need segregated storage and detailed condition notes. Tier 3 is anything above $2,000, requiring full photographic documentation, restricted access, and individual insurance consideration.

Your thresholds might differ based on your market. A store specializing in academic texts might push those numbers higher since their baseline inventory already runs pricier. A general indie bookstore might drop them lower. What matters is consistency — everyone on your team needs to know exactly when a book triggers special handling.

The operational trap here is thinking price alone determines rarity. A $400 book that's readily available from distributors doesn't need the same protection as a $400 out-of-print local history you'll never source again. Build a secondary filter for true scarcity: books you can't reorder, signed editions, local publications with limited runs, or anything with provenance documentation.

Condition documentation that actually holds up in claims

Photographing rare books feels like busywork until you need those photos for an insurance claim. The difference between getting paid and getting denied often comes down to proving pre-damage condition. But most stores either skip photos entirely or take useless ones that don't show what insurers actually need.

Never miss a sale or stock shortage again.

Bookstorely helps you manage inventory, orders, and customer relationships seamlessly.

- Integrated inventory tracking

- Customer purchase history

- Sales reporting & analytics

No credit card required

For books over your Tier 2 threshold, you need five specific angles. Front cover straight-on showing any wear or damage. Spine showing text clarity and binding condition. Back cover for completeness. Copyright page proving edition and printing. One additional shot of any notable flaws — foxing, tears, inscriptions, bookplates. Store these in folders named by ISBN and date, not in random phone galleries where they'll get buried.

For Tier 3 items, back up photos to cloud storage with versioned filenames so they're always discoverable during a claim.

The timing matters as much as the content. Take initial photos during intake, not weeks later when damage might've already occurred. If a book moves between locations — from receiving to the sales floor to an online listing — document each transition. That sounds excessive until you're trying to prove that shipping damage happened after purchase, not while the book sat in your back room.

Written condition notes need to match photographic evidence. Don't just mark "good" or "fair" — write "2-inch closed tear on dust jacket front panel" or "moderate tanning to page edges, text block solid." These details feel pedantic but they're what separate successful claims from denials. Create a condition vocabulary sheet so different staff members describe issues consistently.

For your highest-tier books, consider a quick video showing page-through and all angles. Takes an extra minute but provides undeniable evidence of condition. Store videos separately from photos with clear naming conventions.

Storage segregation and the real cost of mixed inventory

Physical segregation of rare books seems obvious but rarely holds up in practice. Stores start with good intentions — a locked cabinet, a special shelf — then space pressure builds and suddenly that first edition is crammed next to the bargain mysteries because someone needed room for something else.

Your segregation system needs three components: physical separation, visual marking, and access control.

-

Physical separation

-

Visual marking

-

Access control

Keep a small kit of replacement colored stickers and tags near the packing station so mis-tagged items can be corrected immediately.

Physical separation doesn't require a vault, but rare books need designated space that's climate-controlled and away from high-traffic zones. A locked cabinet works for Tier 3 items. Tier 2 can live on regular shelving but in a restricted area — behind the counter, in the back office, anywhere customers can't browse unsupervised.

Visual marking prevents expensive mistakes during busy periods. Use colored shelf tags — red for Tier 3, orange for Tier 2. Add matching stickers to the books themselves, removable but obvious. When someone's rushing through online orders at 4 PM, that orange sticker stops them from tossing a $600 first edition into standard packaging.

Access control isn't about distrust — it's about clarity. List exactly who can handle Tier 3 books without supervision. Usually that's owners and senior staff only. Tier 2 might include experienced full-timers. Everyone else needs oversight. This feels hierarchical until a seasonal employee sells your $3,000 signed Tolkien for cover price because they never checked the system.

The hidden cost of mixed storage goes beyond damage risk. When rare books sit with regular inventory, they get handled more, increasing wear. They're harder to track during inventory counts. They don't get the attention needed for proper online listings. Segregation isn't just protection — it's about giving valuable inventory the operational focus it actually deserves.

Insurance versus self-insurance: the decision matrix nobody teaches you

The insurance question for rare books isn't whether to insure — it's whether to insure externally or self-insure through reserves. Most bookstores get this backwards, over-insuring books that are easy to replace while leaving truly irreplaceable pieces underprotected.

Build your decision matrix around three factors: replacement possibility, claim likelihood, and premium economics. Books you can replace, even with some effort, often make sense to self-insure if they're under $1,000. The premium cost over time exceeds likely losses. Books you'll never find again need external coverage regardless of value — losing them means losing them permanently.

Here's the framework that works for most indie bookstores:

| Book Value | Replaceable | Irreplaceable |

|---|---|---|

| Under $500 | Self-insure | Self-insure with photos |

| $500-1,500 | Self-insure with reserves | Scheduled coverage |

| $1,500-5,000 | Scheduled coverage | Scheduled coverage + agreed value |

| Over $5,000 | Individual policy | Individual policy + agreed value |

Scheduled coverage means adding specific items to your business policy. Costs more than blanket coverage but provides actual protection. Agreed value means the insurer accepts your valuation upfront — crucial for books where market value fluctuates or isn't well-established.

The self-insurance reserve calculation most stores skip: take your total Tier 1 and low Tier 2 inventory value, multiply by 3% (a realistic annual loss rate for careful operations), and keep that as a separate reserve fund. If you've got $20,000 in self-insured rare books, you need roughly $600 in reserves. Seems small, but without it, one bad month of damages wrecks your cash flow.

Track your actual loss rates quarterly. If you're consistently below 3%, your handling protocols are working. Above that means either tighten operations or shift more books to external insurance. The data tells you whether self-insurance makes sense for your specific situation.

The customer damage conversation and when to eat the loss

A customer drops a $400 art book. Water damage appears on a book sold last week. Someone claims they received a damaged first edition you know you shipped in perfect condition. These conversations determine whether you keep customers or create enemies, whether you file claims or absorb losses.

Your first decision point: proving fault versus maintaining the relationship. For books under $200, eating the loss usually makes sense even when the customer caused the damage. The goodwill value exceeds the money. Document everything anyway — photos of returned items, email threads, damage descriptions. You need patterns to spot repeat issues even if you don't pursue individual claims.

For expensive items, your documentation becomes critical. This is where your intake photos pay off. Customer claims damage? Pull the timestamped photos showing perfect condition at shipping. Your packing standards matter here too — if you can show professional packaging, shipping damage becomes carrier liability, not yours.

The conversation that preserves relationships while protecting your business: acknowledge concern, present documentation, offer resolution options. "I understand you're disappointed with the book's condition. Our photos from shipping show it left here without that damage. We can file a carrier claim together, or I can offer you store credit for 20% of the purchase price as a goodwill gesture." Give them agency in the resolution.

Sometimes you eat losses you shouldn't have to. A regular customer who spends $300 monthly gets the benefit of the doubt on a one-time issue. Someone buying their first book from you who immediately claims damage? Document everything and stand firm. The key is having clear policies that flex based on relationship value, not just transaction value.

Set damage allowances in your budget — usually 1–2% of rare book sales covers customer-related losses. Track actual rates monthly. If you're consistently over, either your handling needs work or you're attracting problem customers through certain channels.

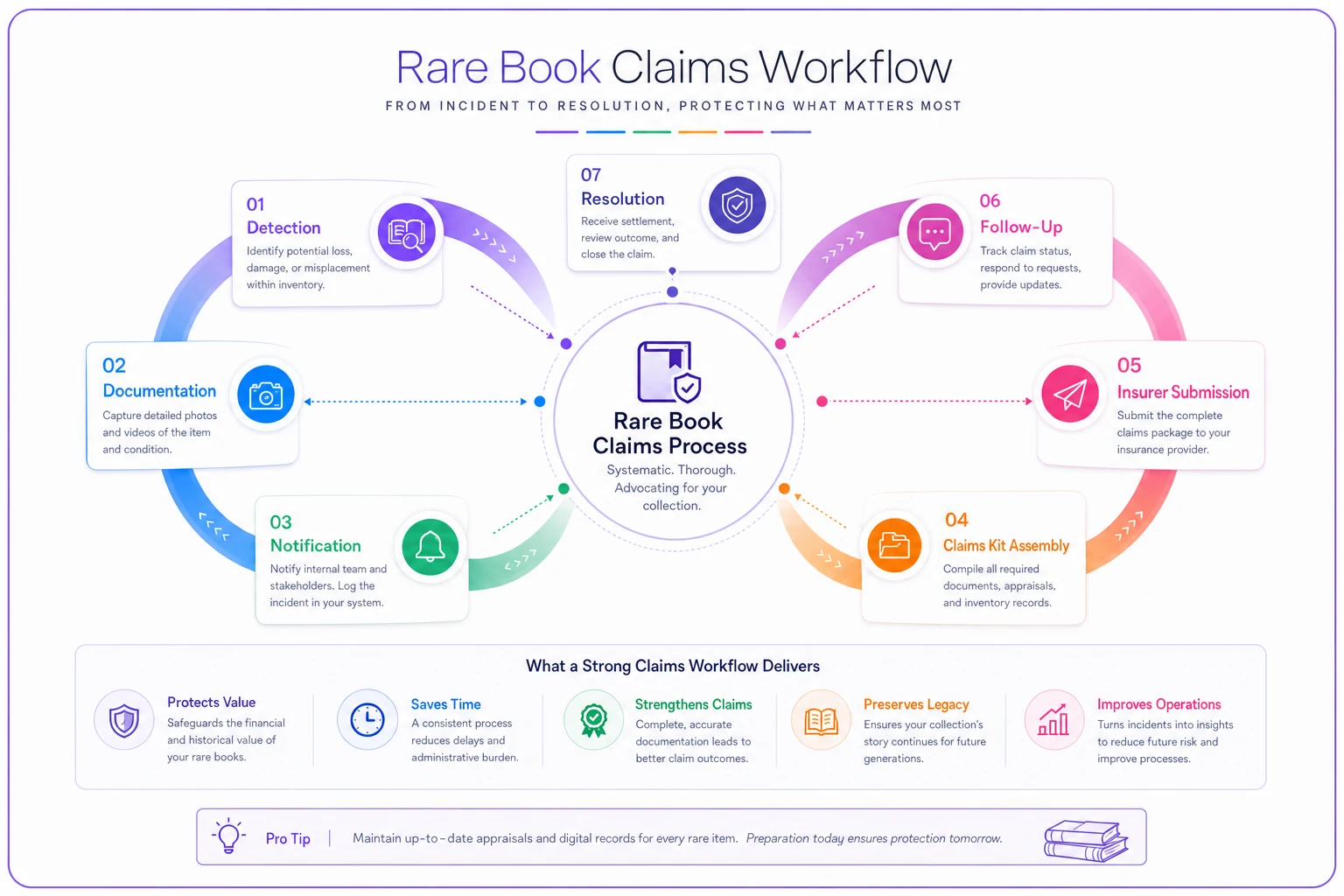

Building the claims workflow before you need it

Insurance claims for rare books fail because stores scramble to create documentation after damage happens. By then it's too late — adjusters want contemporaneous evidence, not reconstructions. Your claims workflow needs to exist before you ever file a claim.

Start with your trigger events. Shipping damage requires carrier documentation within their timeline — usually 24–48 hours. Theft needs police reports immediately. Customer damage gets documented regardless of whether you pursue payment. Water or environmental damage needs photos before any cleanup. Miss these windows and claims get denied on procedural grounds, not merit.

Your claims kit should live in one place, physical or digital. Include insurance policy numbers, agent contact info, photographing guidelines, condition description templates, and carrier claim links. When damage happens, whoever discovers it should document everything immediately, then notify the designated claims person. Usually that's the owner or manager, but vacation coverage matters — someone else needs to know the process cold.

A visual workflow clarifies the steps when a claim occurs.

The documentation package for any claim includes: original intake photos, purchase documentation showing value, current damage photos, written condition comparison, and an incident report. For theft, add police report numbers. For shipping damage, include tracking details and packaging photos. Insurers might not need everything, but having it ready prevents delays.

What actually happens during claims: adjusters question your valuation, challenge condition descriptions, and look for reasons to reduce payouts. Your defense is overwhelming documentation. That $2,000 signed biography? Have the author's website showing signing events, comparable sales from other stores, and condition photos from multiple angles. Make denial harder than approval.

Track claim outcomes in a simple spreadsheet — date, item, claim amount, resolution, time to payment. Patterns emerge quickly. If certain categories consistently get reduced payouts, adjust your coverage or documentation. If claims drag on forever, maybe you need a different insurer. The data helps you optimize both coverage and process.

The recurring maintenance schedule that prevents degradation claims

Rare books deteriorate without proper maintenance, and insurers love denying claims for "gradual deterioration." Your maintenance schedule prevents both the deterioration and the denial excuse.

Monthly tasks take 2–3 hours total. Check climate control in rare book areas — humidity should stay between 30–50%, temperature between 60–70°F. Dust exposed books with a soft brush, moving from top to bottom. Rotate displayed books to prevent uneven light exposure. Update photos for any books showing condition changes.

Quarterly deep maintenance prevents bigger problems. Remove all rare books from shelves, check for pest signs, clean shelving thoroughly. Inspect bindings for loosening, pages for foxing development. Re-photograph your Tier 3 inventory even if condition hasn't changed — insurers appreciate regular documentation. Tighten any protective covers or sleeves.

Annual professional assessments matter for valuable collections. A conservation specialist can evaluate your entire rare inventory for somewhere around $500–1,000. They'll spot issues you'd miss, recommend preventive measures, and provide written assessments that strengthen insurance claims. Think of it as an annual checkup for your most valuable assets.

Document all maintenance in a simple log. Date, task completed, issues found, actions taken. When an adjuster questions why binding damage wasn't prevented, your maintenance log proves professional care. That's often the difference between coverage and denial on gradual damage claims.

The environmental monitoring investment most stores skip: a $50 bluetooth humidity sensor with logging capability. Provides timestamped proof that storage conditions stayed appropriate. When a water damage claim comes in, you can show humidity never spiked, proving sudden event rather than gradual moisture buildup.

Training the reality into your team

Your rare book insurance SOP bookstore protocol only works if your team actually follows it. But training on theoretical damage scenarios doesn't stick. People need to understand the real consequences of skipped steps.

Start with loss stories from your own inventory or the broader industry. The bookstore that lost $30k in water damage because nobody photographed pre-existing conditions. The shop that had theft claims denied because they couldn't prove which editions were taken. Make it real with numbers — a single mishandled $2,000 book can represent a full month of profit for a lot of indie stores.

Role-play the awkward scenarios during slow periods. Customer claims damage on a book sold yesterday — walk through pulling documentation, having the conversation, making the judgment call. Package a mock rare book for shipping while someone watches and critiques. Practice makes the real moments less stressful.

The documentation drill that builds habits: once a month, grab three random rare books and have staff complete full documentation in 15 minutes. Photos from all angles, written condition notes, proper filing. Time pressure reveals who actually understands the system. Winners get coffee gift cards or first choice of advance reader copies.

Create laminated reference cards for quick decisions. Tier thresholds, photo angles required, who to notify for claims. Hang them where rare book processing happens. Nobody memorizes everything, but everyone should know where to find answers fast.

Cross-training matters more for rare books than regular inventory. When your rare book expert takes vacation, someone else needs to handle that $5,000 collection that walks in. Rotate responsibilities monthly so multiple people stay current on protocols. Redundancy prevents expensive mistakes.

Inventory auditing and the surprises that surface

Regular audits of your rare book inventory reveal problems before they become disasters. Books miscategorized as regular stock. Valuable items without documentation. Conditions that degraded without anyone noticing.

Run a full rare book audit quarterly, separate from regular inventory counts. Pull every book above your threshold, verify its documentation exists, check current condition against what was recorded. Takes a full day for most stores but surfaces things worth finding. That signed poetry collection marked as a $30 regular hardcover. The first edition showing foxing that wasn't there three months ago.

The audit checklist that catches everything: physical location matches system location, photos exist and are findable, condition notes match current state, insurance category is appropriate, pricing reflects current market. Each discrepancy gets logged and corrected immediately, not "when things slow down."

Audit results feed back into your process. If books repeatedly get miscategorized, your intake workflow needs work. If conditions degrade faster than expected, check environmental controls. If documentation keeps going missing, fix your filing system. The audit isn't just about finding problems — it's about fixing the intake process that created them.

Random spot-checks between full audits keep everyone honest. Grab five rare books weekly, verify their documentation. Takes 10 minutes but maintains standards. Staff knows checks happen regularly, so they maintain protocols even during the busy rushes.

Making the economic case and measuring what matters

Your rare book protocols need to prove their value. Track the right metrics and the ROI becomes obvious. Track the wrong ones and it looks like bureaucratic overhead.

The core metric: loss rate as a percentage of rare book revenue. If you're doing $50k annually in rare books and losing $2k to damage, theft, and claims issues, that's 4%. Stores with solid protocols tend to run 2–3%. Stores without them often land at 5–8%. Dropping from 6% to 2% on $50k in sales recovers $2k in margin — likely more than the protocols cost to implement.

Time investment matters too. Document how long tasks actually take. Initial photo documentation: roughly 3 minutes per book. Maintenance checks: about 2 hours monthly. Filing a claim with proper documentation: 1 hour. Filing without it: 3–4 hours plus a lower success rate. The upfront time pays off.

Customer satisfaction around rare books differs from regular inventory. Track specific feedback about rare book handling, packaging, condition accuracy. Buyers spending $500 on a first edition expect a different experience than someone buying a $15 paperback. Their positive reviews drive more rare book sales.

The hidden value most stores overlook: rare books as marketing assets. That $3,000 signed collection brings foot traffic even if it doesn't sell immediately. People share photos, tell friends, create real buzz. Track store visits and social engagement around rare book announcements. Often the marketing value exceeds the margin.

Insurance premium savings from good documentation and low loss rates can reach 15–20% annually. Insurers price based on risk. Show consistent protocols, low loss rates, and professional documentation — premiums drop. That's direct bottom-line improvement from operational discipline.

Software coordination and the automation opportunities

The manual nature of rare book protocols creates natural opportunities for automation, especially around documentation and workflow triggers. Judgment calls stay human. The administrative burden doesn't have to.

Automated threshold alerts prevent expensive books from disappearing into regular inventory. When someone enters a book above your price threshold, the system flags it for rare book protocols immediately. No more discovering that first edition got processed as a standard hardcover.

Photo storage and organization becomes manageable with proper folder structures and naming conventions. Automated backup ensures documentation survives local computer failures. Cloud storage with consistent organization means anyone can find the photos they need during a claim, not just the person who originally took them.

Workflow automation reduces skipped steps. Book enters system above threshold → task created for photo documentation → photos uploaded → condition notes required before the listing goes live. Each step links to the next, preventing shortcuts during busy periods.

The insurance renewal process gets easier with organized documentation. Instead of scrambling to pull inventory lists and valuations, run a report showing all rare books, their documentation status, and current market values. What used to take days takes minutes.

Maintenance scheduling moves from memory to system. Monthly reminder for climate checks and dusting. Quarterly alert for deep cleaning and inspection. Annual prompt for professional assessment. The system tracks it so people don't have to carry it in their heads.

The coordination between rare book protocols and other operations matters too. Packing standards need to flag special handling. Online listings should automatically include condition photos. Purchase orders might need to bypass rare books entirely to prevent automated reordering of one-of-a-kind items.

The bottom line on protecting valuable inventory

Running rare book protocols feels like overhead until something expensive goes wrong. Then suddenly everyone wishes there had been proper documentation, clear thresholds, and trained staff in place. The stores that do well with rare books aren't necessarily the ones with the most valuable inventory — they're the ones that treat that inventory with operational respect.

Your rare book insurance SOP bookstore system doesn't need to be complicated. Define clear thresholds, document conditions properly, segregate inventory physically, and train your team on real consequences. The time investment pays off in reduced losses, successful claims, and customer trust.

Most importantly, measure what you're doing. Track loss rates, claim success rates, and time investments. Let the data guide your decisions about insurance versus self-insurance, protocol adjustments, and where to allocate resources. Rare books can be genuinely profitable — but only if you protect that profit through consistent operational discipline.

Ready to elevate your bookstore’s operations?

Join 500+ bookstores using Bookstorely to boost sales, optimize stock, and delight book lovers.